The Unraveling

How housing became unaffordable, savings became pointless, children became unthinkable, and a generation lost faith in the system.

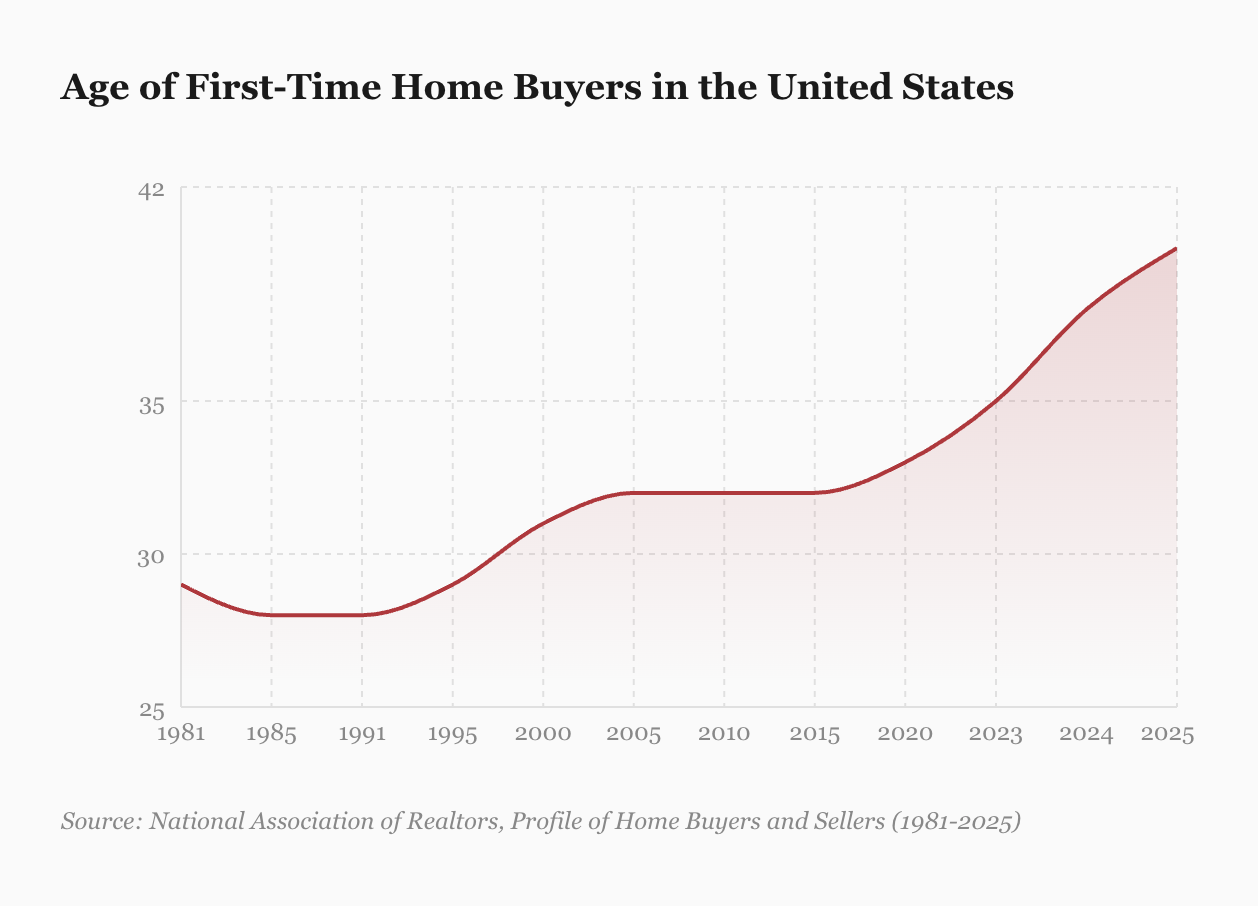

In 1991, the typical first-time homebuyer in America was 28 years old. They had been out of college for a few years, maybe married, starting to build a life. The path was clear: work hard, save up, buy a home, start a family, build wealth, retire with dignity.

In 2025, the typical first-time homebuyer is 40. They have been out of college for nearly two decades. They are closer to the age when they can collect Social Security than they are to their graduation day.

This is not a story about inflation, though inflation made it worse. This is not a story about interest rates, though they compound the problem. This is a story about what happens when an entire generation is locked out of the basic economic machinery that previous generations took for granted—and what they do when they realize the door is never going to open.

Age of First-Time Home Buyers

The Door That Closed

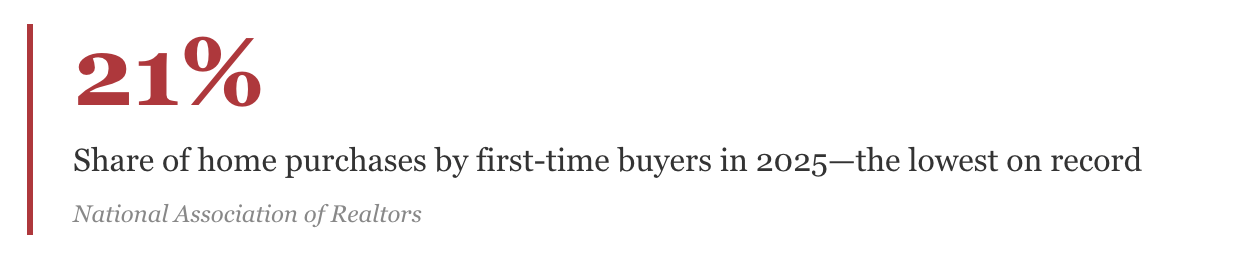

The numbers tell a story that feels almost unbelievable until you live it. In 2025, first-time buyers made up just 21% of all home purchases—the lowest share ever recorded since tracking began in 1981. The typical first-time buyer now needs a household income of $97,000 just to qualify, up $26,000 in just two years.

A record 26% of home purchases are now made entirely in cash. The market has split in two: current homeowners, sitting on trillions in equity, trading properties among themselves—and everyone else, watching from the outside.

“The first-time homebuyer who can enter into today’s market is older, has a higher income, and is wealthier,” Jessica Lautz, deputy chief economist at the National Association of Realtors, told reporters. She was describing not opportunity, but its absence. The only people who can get in are those who were already ahead.

The Logic of Not Saving

When you cannot afford a home, what exactly are you saving for?

This is the question that haunts the financial lives of young Americans. A 2024 Harris Poll found that 46% of Gen Z agreed with this statement: “No matter how hard I work, I will never be able to afford a home I really love.” Researchers at Northwestern and the University of Chicago have a term for what happens next: they call it “giving up.”

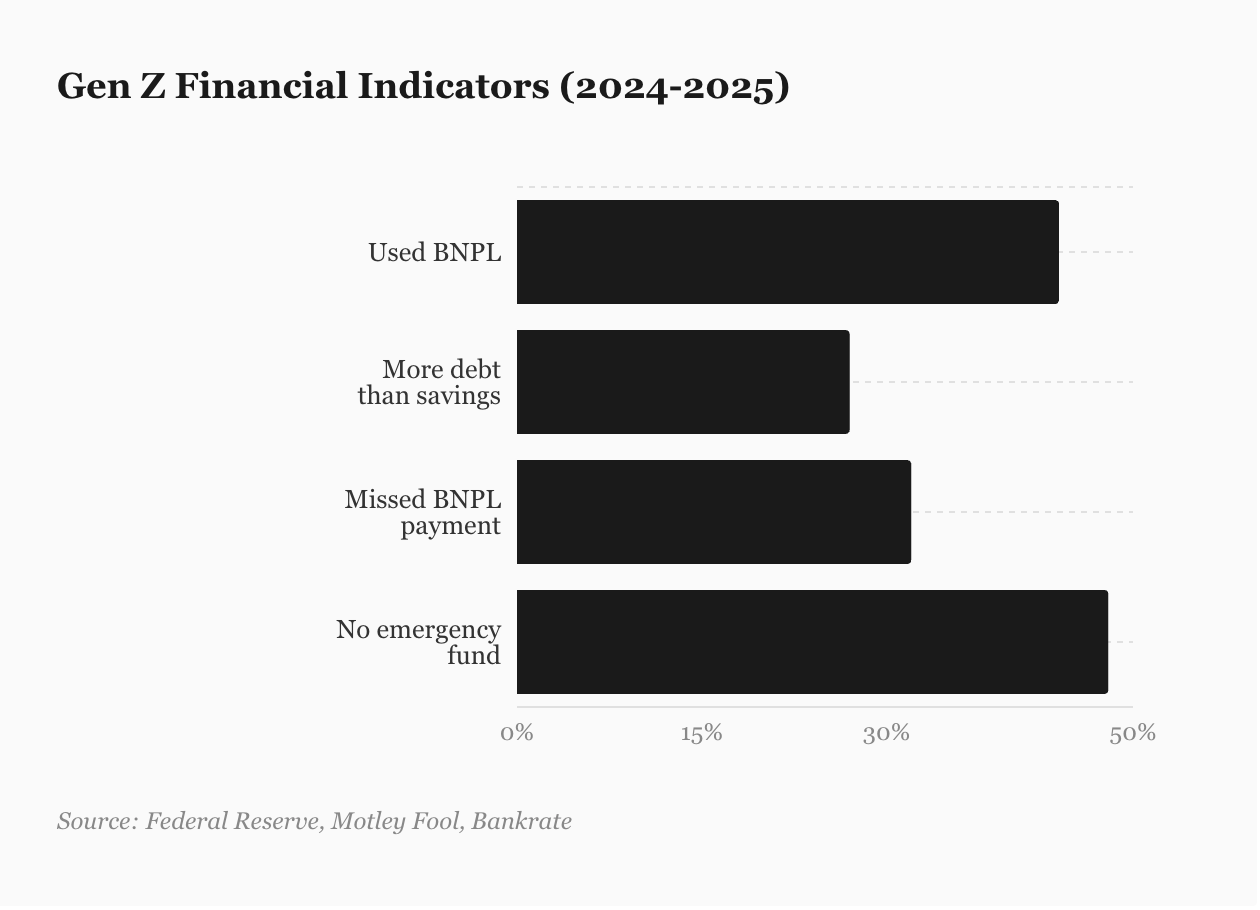

The data shows what giving up looks like. Nearly half of Gen Z—44%—used Buy Now, Pay Later services last year. One in four carries more debt than savings. A third have missed payments. Almost half have no emergency fund at all.

Gen Z Financial Indicators

Economists call it “financial nihilism.” Young people call it being realistic. When you split a $40 meal into four payments, you are not being irresponsible. You are adapting to an economy where your paycheck does not stretch to the end of the month, where traditional milestones are permanently out of reach, where the future feels like someone else’s problem because it was never going to be yours anyway.

The Children Who Were Never Born

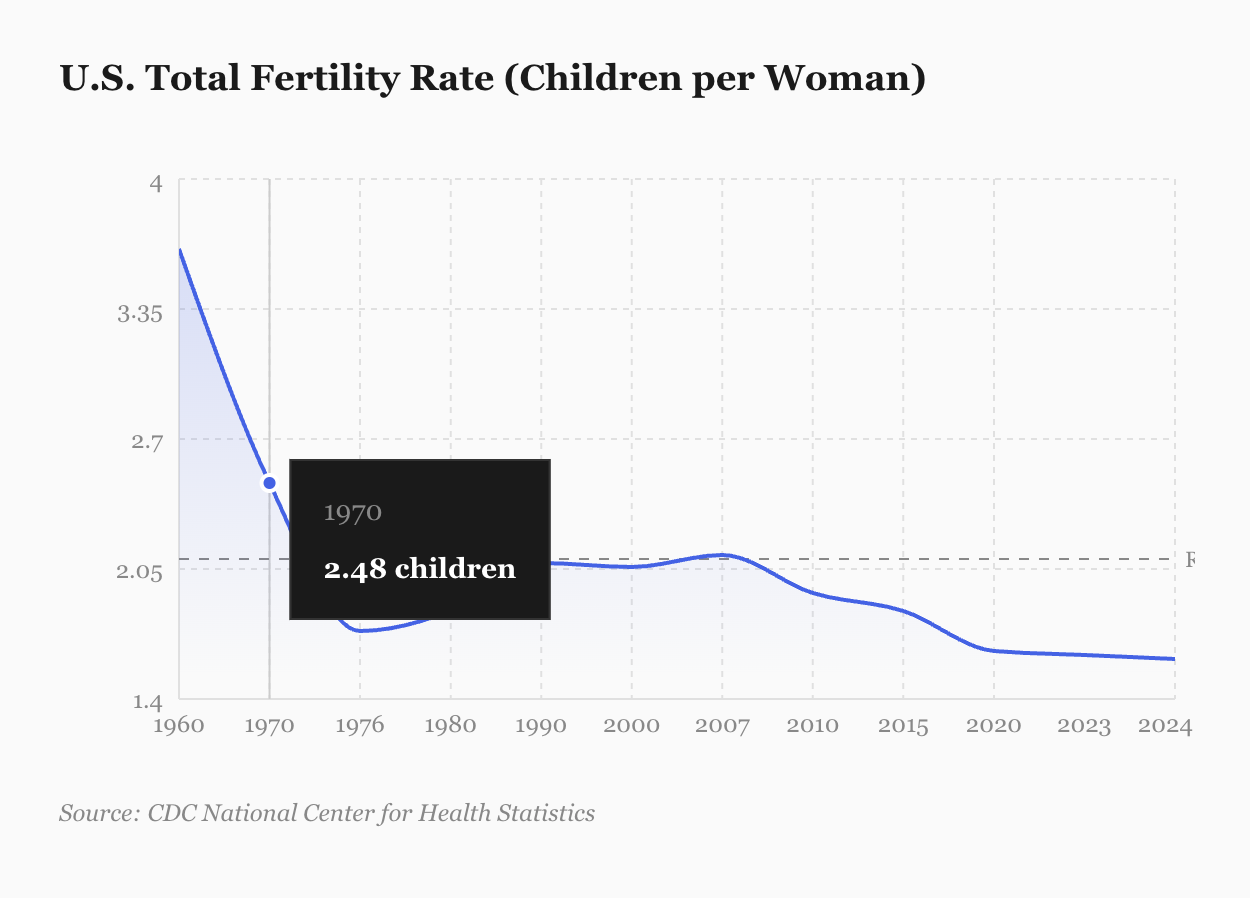

In 2024, the U.S. fertility rate fell to 1.599 children per woman—the lowest in American history. The number needed to maintain population without immigration is 2.1. We have been below that threshold, with brief exceptions, since the early 1970s.

U.S. Fertility Rate (Children per Woman)

Politicians speak of this as a crisis of values or a problem of access to fertility treatments. The data suggests something simpler: people are not having children because they cannot afford to.

“Worry is not a good moment to have kids,” Karen Guzzo, director of the Carolina Population Center at UNC, told CBS News. “And that’s why birth rates in most age groups are not improving.”

Housing researchers describe unaffordability as a “fertility tax” on young non-owners. When you cannot buy a home, you delay marriage. When you delay marriage, you delay children. When you delay children long enough, you do not have them at all.

The Search for Someone to Blame

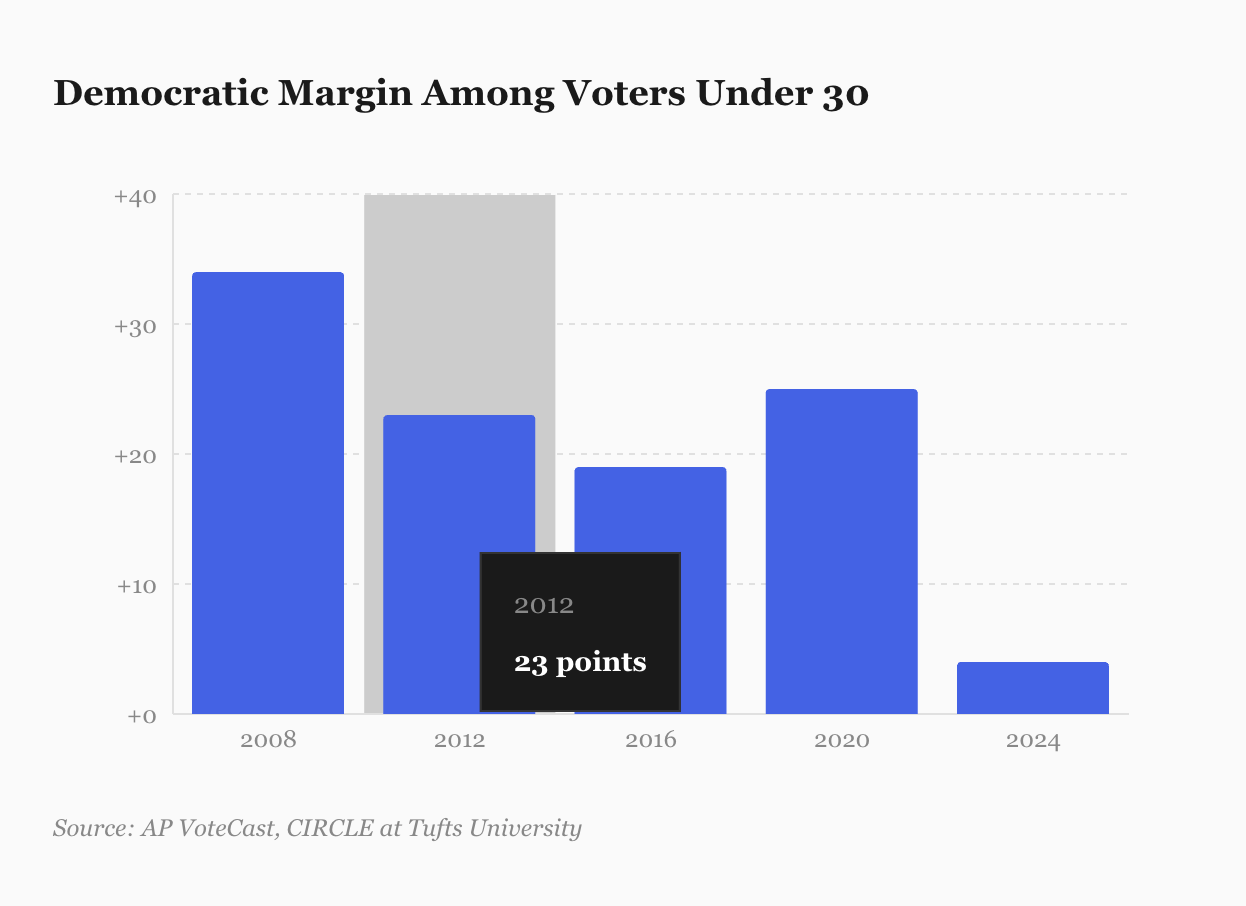

In 2020, voters under 30 favored Joe Biden over Donald Trump by 25 percentage points. In 2024, that margin collapsed to just 4 points for Kamala Harris. It was the strongest showing for a Republican presidential candidate among young voters since 2008.

Democratic Margin Among Voters Under 30

The shift was especially pronounced among young men. Young women remain reliably liberal. Young men are moving right at speed—not toward traditional conservatism, but toward something angrier and less defined. When researchers at CIRCLE analyzed young Trump voters, they found that only 51% believed the government was “doing too many things better left to businesses.” The rest wanted more government intervention. They are not ideological conservatives. They are people who want something to change.

Research from Oxford and other institutions has documented how housing inequality drives populist voting on both the left and the right. When house prices surge in one area and stagnate in another, the people in the stagnant area do not simply accept their fate. They vote against whoever is in power. They vote for anyone who promises disruption.

Young liberals say their views on social issues have moved “much more” to the left. Young conservatives report moving further right on both economic and social issues. The center is emptying out. Researchers at Berkeley describe young voters of all ideologies as increasingly “fatalistic”—convinced that institutions cannot solve problems, that the game is rigged, that the only question is who rigged it.

The Ladder That Disappeared

Now consider what happens when you remove the first rung.

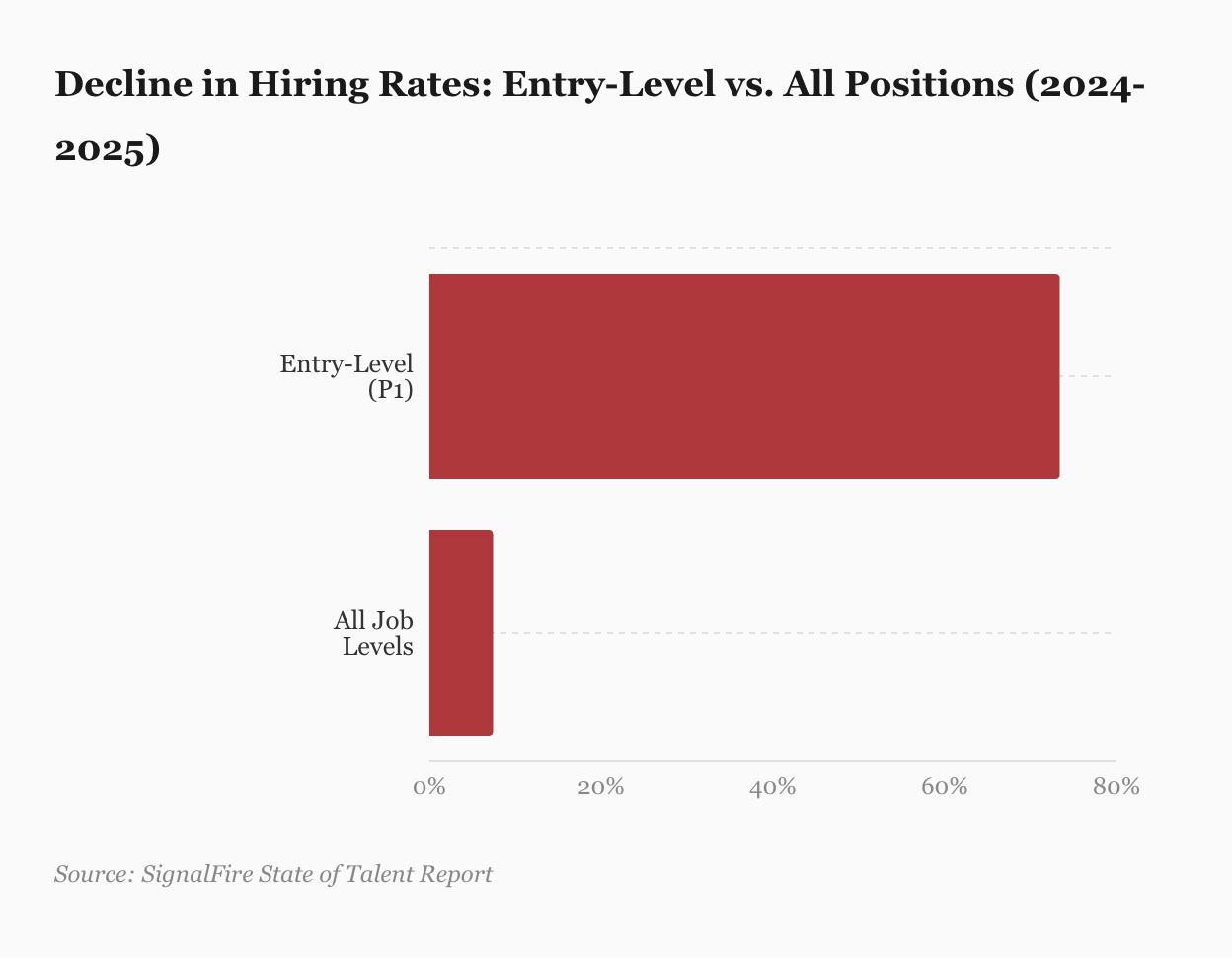

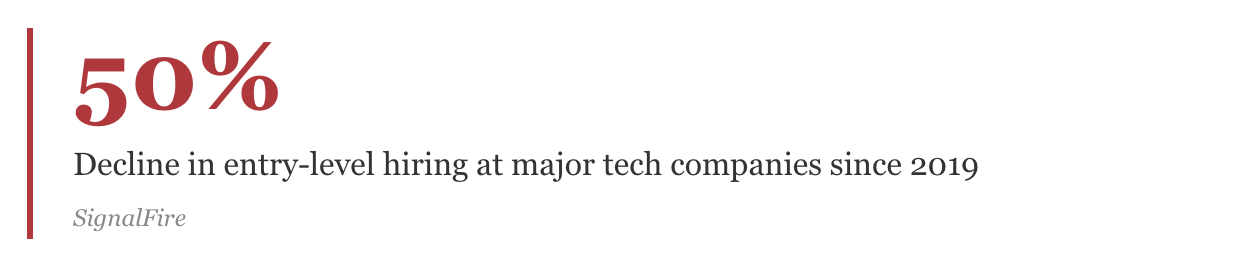

A study by SignalFire, tracking 650 million professionals across 80 million organizations, found that entry-level hiring at major tech companies has fallen by more than 50% since 2019. By 2024, recent graduates made up just 7% of new hires at Big Tech firms—half the pre-pandemic level. The World Economic Forum’s Future of Jobs Report found that 40% of employers expect to reduce staff in roles where AI can automate tasks.

Decline in Hiring Rates (2024-2025)

The pattern is consistent across industries. Job platforms reported a 35% decline in junior tech positions across major EU countries in 2024. Indian IT services companies have reduced entry-level roles by 20-25% due to automation. Entry-level job postings in the U.S. fell 35% between January 2023 and June 2025.

The jobs being eliminated are precisely the ones that young people relied on to gain experience: debugging code, reviewing documents, compiling reports, handling customer service, conducting basic research. These tasks are now automated. The work that remains requires experience that can only be gained by doing work that no longer exists.

| Statistic | Verified Figure | Source |

| Professional Dataset | 650M professionals / 80M orgs | SignalFire Beacon Data |

| Entry-Level Decline | >50% drop since 2019 | SignalFire State of Talent 2025 |

| Grads as % of Hires | 7% (in 2024) | SignalFire State of Talent 2025 |

| AI Staff Reduction | 40% of employers | WEF Future of Jobs Report 2025 |

“The loss of clear entry points doesn’t just shrink opportunities for new grads,” Heather Doshay of SignalFire told researchers. “It reshapes how organizations grow talent from within.”

Universities have begun striking deals with AI companies to train students on tools that may eliminate the jobs those students are training for. A generation is being asked to pay for credentials that provide access to a door that is closing.

What Breaks

There is a social contract at the heart of market economies. Work hard. Play by the rules. Delay gratification. In return, you get stability, a stake in the system, a reason to care about its continuation.

That contract is breaking. Not because young people have different values or weaker character. Because the terms have changed and no one acknowledged it. Work hard, and you still cannot afford a home. Play by the rules, and the entry-level job disappears. Delay gratification, and watch the goalpost move further away.

When people have no stake in a system, they stop defending it. They spend instead of save, because saving does not lead anywhere. They do not have children, because they cannot afford to raise them. They vote for disruption, because stability has given them nothing. They look for someone to blame—immigrants, elites, corporations, the other party—because the truth is more complicated and offers no clear enemy.

The truth is that the economic machinery that built the middle class is seizing up. Housing policy, wage stagnation, the cost of healthcare and education, the structure of labor markets, the displacement of entry-level work—these are not culture war issues. They are system failures. And system failures do not care about your politics.

A first-time homebuyer in 1991 was 28. A first-time homebuyer in 2025 is 40. Somewhere in those twelve years is everything we have lost.

Data sources include the National Association of Realtors, CDC National Center for Health Statistics, Federal Reserve, Consumer Financial Protection Bureau, SignalFire, Revelio Labs, World Economic Forum, AP VoteCast, CIRCLE at Tufts University, and peer-reviewed research published in the British Journal of Political Science, Journal of Economic Geography, and the American Journal of Political Science.